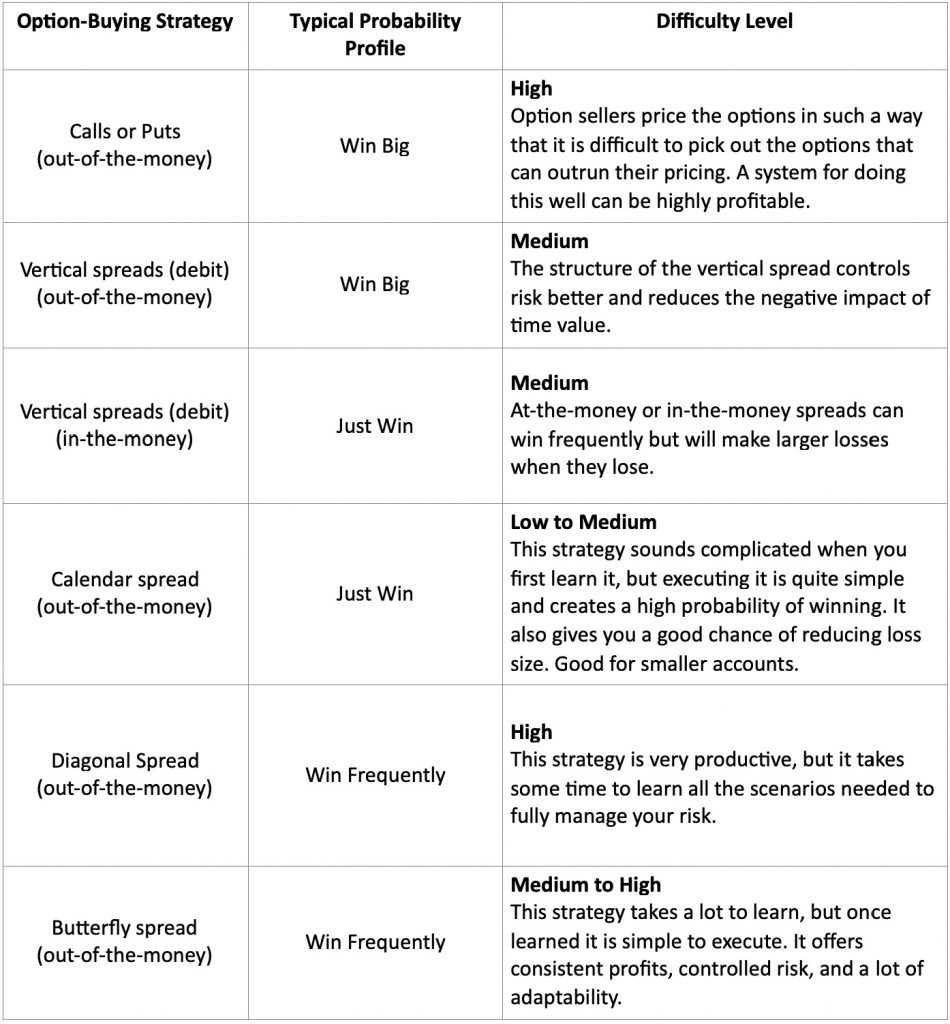

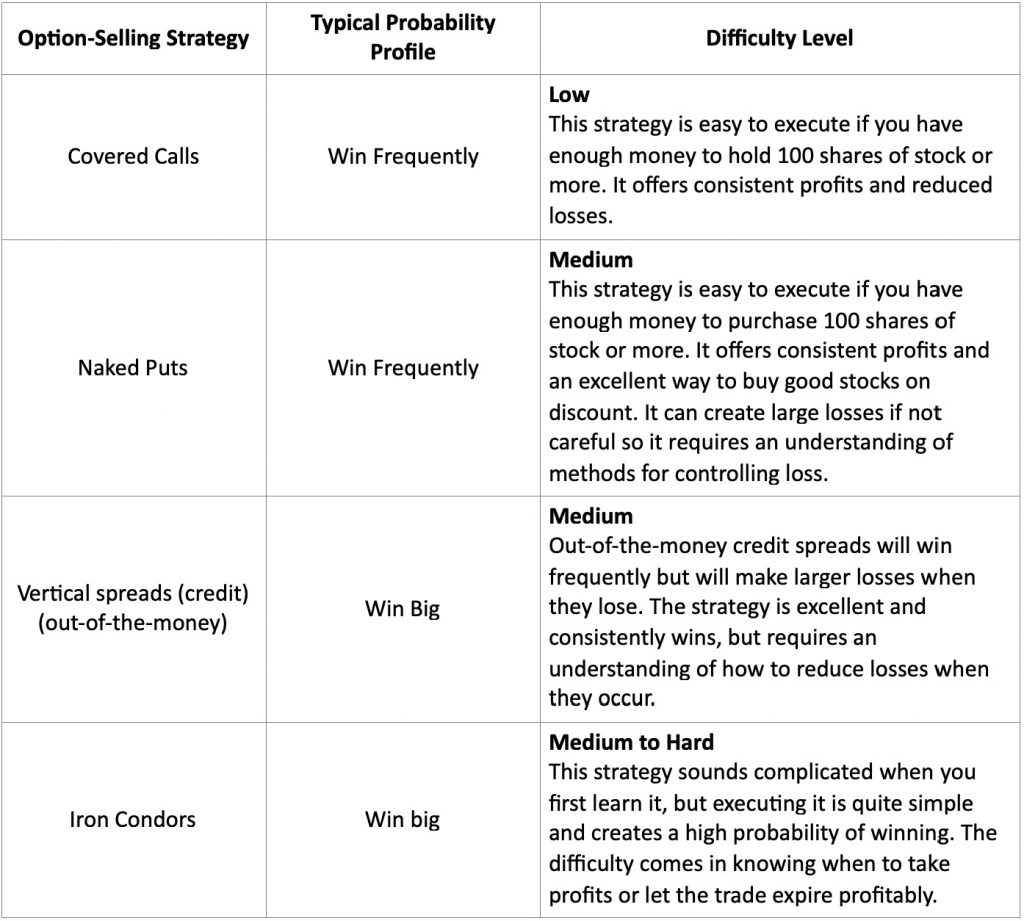

Improve Results with Options

Options are instruments of probability. They are priced using a complex mathematical formula which boils down to the measurement of two variables: (1) Intrinsic value (or how much “in the money” it is), and (2) ‘Time and Probability’ value (most commonly just known as time value). Understanding these two variables is key to trading options profitably.

Far too many traders lose money simply because they don’t understand how market makers adjust option pricing in their own favor. The following simple truths about option pricing will help you recognize where option prices are likely to end up, and the probabilities associated with that final outcome.

- Option prices are set by option market makers.

- Options are priced so they decrease in value more often than they rise.

- The option market maker adjusts the price of the option to make it likely they’ll win 70% of the time.

Because these concepts are true, they lead to three important trading corollaries:

- Option sellers have a higher probability of winning but are guaranteed smaller profits in comparison to the risks they take on each trade.

- Options buyers profit only if the underlying rises fast enough for the intrinsic value part of the option’s price to offset the loss of time value as time passes.

- Option buyers have a lower probability of winning compared to option sellers, but make much larger percentage gains when they do win.

This lesson will explore each of these simple truths and their corollaries to help you understand how you can use the probability profiles and trading edge you learned in previous lessons to maximize profits in your option trading.

Truth #1: Option Prices are Set by the Market Makers

Option market makers use a Nobel prize winning formula and fast computer technology to help them make a market in the derivatives known as options. This formula incorporates many variables which can be boiled down into just two basic components: Intrinsic value and time value.

Intrinsic value is determined by the relationship of the option’s strike price to the underlying’s current price. Intrinsic value moves dollar for dollar as the underlying moves. Meaning if the underlying goes up $1, the call option’s intrinsic value will also go up $1. If the underlying falls in value, the intrinsic value of the call option falls at exactly the same rate. Put options are the opposite. If the underlying drops $1 in value, a put option’s intrinsic value will rise $1 and if the underlying rises in value by $1, the intrinsic value of the put option drops $1. Intrinsic value will always either be positive or zero.

The time value (not the intrinsic value) portion of an option’s price is where the market maker adjusts the price to insure they keep their probable winning percentage at 70%. This means the market maker will inflate or deflate the price of time in response to changes in both the macro environment and conditions of the underlying equity. Time value is also a decaying asset because it loses value as time passes. Therefore, time value both fluctuates and constantly decays as time passes and will eventually be worth zero at expiration.

If expectations are high that the underlying will increase in volatility (like around earnings), market makers raise the price of time to keep their expected winning percentage at 70%. The converse is also true, they’ll reduce what they charge for time during periods of lower volatility. More advanced traders and strategies make use of these factors that affect the price of time and as you gain in experience, you may find a need to learn these advanced features. But for now, the simple approach is to understand time both fluctuates in price and decays in value with each passing day and will eventually be worth nothing on expiration.

Trading stock differs from trading with options because options have more moving parts such as expirations dates, puts versus calls, a wide variety of strategies and the impact on time value from market expectations. The two biggest risks to those who trade option is expiration date (the option eventually expires) and time decay. Not only does a person need to keep track of direction (up vs. down), but they must also keep an eye on all these other factors. Some have compared stock trading to the game of checkers and options trading to chess—and rightly so.

This module will help you better understand the two primary ways to open an options position: Either as a buyer (speculator), or as a seller (cash flow generator). Time decay works against a buyer and for a seller. You can be either (or both) an options buyer or seller depending on the strategy you choose. Understanding how options are priced helps you select the best option strategy to implement based on your probability profile, your forecast, and your system.

Time Value and Intrinsic Value

Intrinsic value

While it is true that you don’t need to understand the Nobel-prize-winning math that drives option pricing, it is also true that traders can gain an edge by understanding a few basic components of that math.

Whether demand is high or low, the option market makers constantly strive to make their price reflect the right value based on potential opportunity and time left before expiration. This value can be sorted into two important components: Intrinsic value and Extrinsic value.

The most important variable you need to understand is the fluctuating nature of the value of time and the continual erosion of its value each passing day. Time loses value faster as an option approaches its expiration. For an option to be profitable on expiration, any loss of time value must be recouped by an increase in the option’s intrinsic value.

Intrinsic value is measured as the difference between the strike price and the actual price of the stock. Call options have intrinsic value if the strike price of the contract is lower than the current stock price. Put options have intrinsic value if the strike price is higher than the current stock price. Strike prices that have intrinsic value are referred to as “in-the-money” options.

On the other hand, call options with a strike price above the currently traded stock price have zero intrinsic value. Same with put options that have a strike lower than the current price of the stock. These kinds of options are referred to as “out-of-the-money” options.

The premium for in-the-money options have both intrinsic and time value components. By contrast, out-of-the-money options have only a time value component, so they are much more susceptible to time decay.

Extrinsic value

The second important component which determines the price of an option is extrinsic— or time— value. Time value is interesting because it both constantly decays and can also become more or less expensive, depending on demand.

The time value represents a mathematical calculation about how much the underlying could move given the amount of time left before expiration. The time value of an option is established by an option seller’s pricing model which includes traders’ expectations about what will happen with the stock. It also includes the perception of what the stock has done in the past, and what it might do in the near future. The price also includes a measure of how much the stock may move within a given day. Lastly it includes and a valuation of the alternatives to any option trading (such as interest rates on bonds).

This mathematical model includes everything that goes into pricing an option except its intrinsic value. Professional option market makers refer to this combination of factors as implied volatility. We’ve referred to it simply as time value. Whatever you choose to call it, remember that it can fluctuate and become more or less expensive due to market conditions, that it decays in value over time, and that it always works against an option buyer and for an option seller.

In contrast to the complexity of determining the value of time, the intrinsic value is the “in-the-money” value of the option. It is easily calculated as the difference between the stock price and the value of an option’s strike price. For example, if a Call option gave you the right to buy the stock at a strike price of $40, and the equity currently trades at $42.23, then your option would have an intrinsic value of $2.23 ($42.23 current price – $40 right to buy price = $2.23 of intrinsic value). If the option cost $5.43, then time value would be $3.20 ($5.43 price of the option – $2.23 intrinsic value = $3.20 time value). On the other hand, a put option in this example would have zero intrinsic value ($40 right to sell price – $42.23 current price = -$2.23…a negative intrinsic value is automatically set to zero). If the $40 put option cost $3.20, the entire price is time value since the put option is out-of-the-money.

If the equity increases in price to $45 at expiration, the intrinsic value increases exactly as you might expect, penny for penny; while the time portion of the option’s price would continue to fluctuate based on market conditions and also constantly erode until expiration when it reaches zero.

The only way for this (or any) option to be profitable on expiration is for the in-the-money value to move more than the amount of extrinsic (time) value lost to the passage of time — $3.20(in the put option example above.

Changes in time and intrinsic value

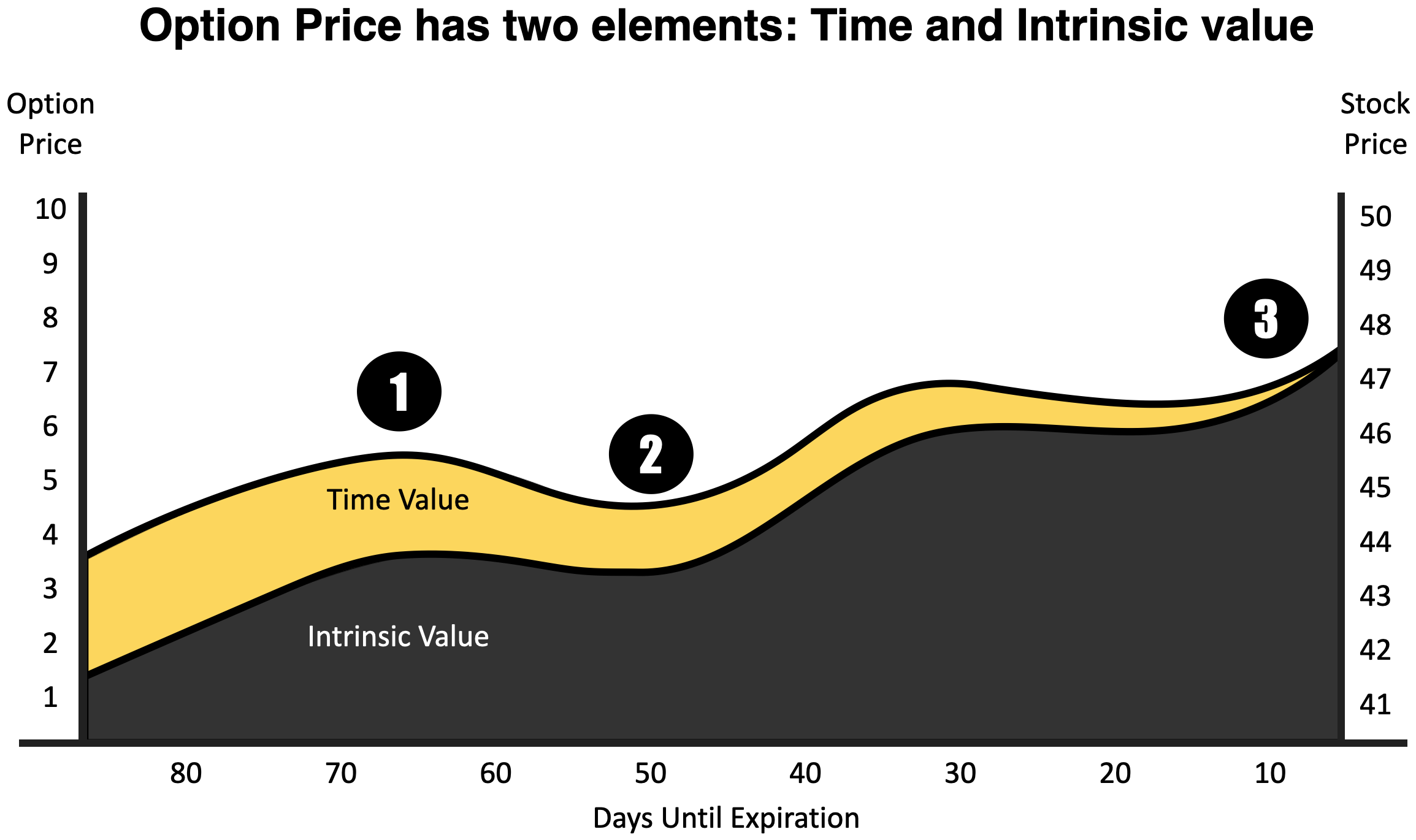

Understanding changes in time value is a different matter from changes to intrinsic value. If the stock value goes up $1.00, the intrinsic value increases by one dollar, but the time value will most likely decrease, both with the passage of time and also with the rise of the stock. This means your option will not always rise in a dollar-for-dollar pace. At times it may go up with a rise in the stock, but at a disappointingly slow rate. The following figure demonstrates how it the price of the option changes over time in comparison to the stock price. The intrinsic value is depicted in black, while the time value is depicted in yellow.

In this figure hypothetical stock and option prices are depicted over the course of 90 days. The price of the stock begins at $42.75 and fluctuates upward until expiration day when it happens to close at $47.75.

The option depicted here is a call option with a $40 strike price and an expiration date 90 days from the start of the graph. This chart attempts to demonstrate how the stock and option prices vary in a related fashion over time. Notice four important concepts shown in this figure:

- Over the course of 90 days, the time value—depicted in yellow—diminishes.

- At times the stock price may hold steady, but the option price will fall relative to the stock (as depicted between point ① and ②.

- Towards the end of expiration, as depicted near point ③, the option price moves in close tandem to the stock price. This assumes that the option price has some intrinsic value.

- Option pricing works efficiently when the price of the stock and the price of the option do not vary greatly, as depicted between points ② and ③.

When you can perceive this change to the extrinsic value over time, you can see more clearly why the three truths about options are consistently apparent in the options market.

Options can be bought and sold at any time, it is not necessary to wait until expiration before selling a profitable option. In fact, it is often better not to wait until expiration before liquidating your option positions. Using this losing trade as an example, it is very possible that the equity moved around enough before all of the time value decayed for this option to have been profitable at some point during its lifespan.

Truth #2: Options Are Priced so That They Decrease in Value More Often Than They Rise

Truth #3: Option Market Makers Price the Option to Win 70% of the Time

These two truths are closely related so we’ve combined them into one discussion. The truth is options are not like stock. A stock buyer can hold the stock forever. Options traders don’t have that luxury. Stock buyers can set stop losses and profit targets to give them a mathematically proven statistical base winning percentage. Options traders don’t have that luxury. The initial price of an option is set by (and in favor of) the market maker and the reality that time value decays and the option will eventually expire present real danger to option traders.

But, options also present such an exciting and potentially lucrative range of possibilities for profit that every investor and trader should make implementing them a priority. Any percentage move in the stock creates a much bigger percentage move in the option. Option buyers put less money into the trade (risk less) and have the potential to make a large multiple on any move in the underlying makes in the desired direction.

Additionally, options give people strategies to take advantage of every kind of market. There are cash flow strategies, market neutral strategies, protection strategies and speculation strategies. Each of these strategies key in on the corollaries mentioned above:

- Option sellers have a higher probability of winning but are guaranteed smaller profits in comparison to the risks they take on each trade.

- Options buyers profit only if the underlying rises fast enough that the gain in the intrinsic value part of the option offsets the losses of time fluctuation and time decay.

- Option buyers have a lower probability of winning compared to option sellers, but make much larger percentage gains when they do win.

These corollaries align well with the probability profiles discussed in the lesson titled, “Select a strategic approach.” The Win Frequent probability profile often employs option selling strategies. The Win Big probability profile often employs option buying strategies. The Just Win probability profile is flexible enough to enter trades either as a buyer or a seller. Future lessons will explore the risks and rewards option buyers and sellers both face as they implement the various strategies you’ll learn through your curriculum.

Risks and rewards for the option buyer